The paper Prof. Johannes Schmidt (Karlsruhe) first presented at our Seminar “Introduction to New European Political Economics” at BI Norwegian Business School (see overview , video recordings of all presentations, and background reading) in November 2017 has now been published in the European Journal for the History of Economic Thought, Volume 26, 2019 – Issue 6:

Its title is “Balance Mechanics and Business Cycles“: read it by clicking here. Watch the video of Johannes Schmidt’s Oslo presentation of this paper by clicking here.

Schmidt lays out how Wolfgang Stützel offers an overall shared framework (based on law and a specified sectoral accounting model of a closed economy) within which both orthodox “real” and orthodox and heterodox “monetary” theories of business cycles can be meaningfully related to one another. By relating both views back to the general framework, the special areas of applicability of the cases described by orthodox and heterodox models, as well as orthodox and heterodox overgeneralizations, can be clearly identified, so that their seeming incommensurability is replaced by an integrated view. This view precisely identifies where each theory has its rightful place and where it overgeneralizes, therefore needs to be corrected. Rather than vague “tolerant” pluralism or a confrontative view of “incommensurability” of orthodox and heterodox models, this straightforward approach aims at (and, in our view, offers) integrative progress in both the Keynes’ (GT Chap. 1) and Thomas S. Kuhn’s sense. This was Stützels general methodological strategy. He also used it to formulate a general theory of valueing and pricing, including the previous theories as special cases.

In presenting the monetary aspects of Stützel’s theory of business cycles, Schmidt demonstrates this for theories that deal with “money” in different ways: (1) Walrasian tradition “real business cycle” theories, (2) theories based on some form of the quantity theory of money (such as monetarism or today’s “100% money” proposals, (3) Post Keynesian (including Minskyan) “monetary production” models and (4) New Keynesian models.

To put Schmidt’s paper in context, it may be helpful to watch the previous presentations of the seminar, especially Nicolas Hofer’s presentation of the “bipartite division of monetary theory” into stocks/flows of means of payment vs. stocks/flows of net financial assets (see here) and Thomas Weiss’ presentation of Part I of Stützel’s theory of business cycles, covering aggregate demand/supply constellations and how their effects differ when they hit upon existing market tensions: buyer’s vs. seller’s markets (see here).

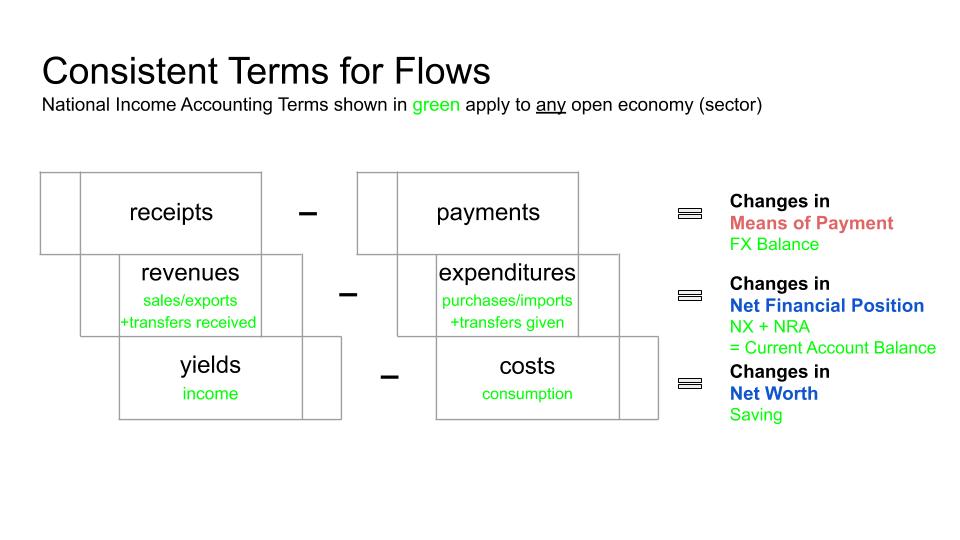

The accounting relationships presupposed there will be familiar to MMTers, but get crucially more specific, precisely distinguishing three types of flows of monetary wealth, thereby introducing the bipartite division of the theory of money into stocks/flows of (1) means of payment and (2) net financial assets (aka financial net worth), the latter representing the crucial “missing link” between the “monetary” sphere of financial assets/debt and “real” sphere of nonfinancial assets. Stützel adopted this distinction of three types of flows of monetary wealth from standard german business accounting; it was originally developed as a financial accounting concept for business accounting by Eugen Schmalenbach and is known as the ‘Schmalenbach-Staircase’ (for the shape of its geometrical depiction):

It is also described in more detail in Johannes Schmidt’s 2015 paper, “Reforming the Undergraduate Macroeconomics Curriculum: The Case for a Thorough Treatment of Accounting Relationships” (pdf here) and Fabian Lindner’s 2012 paper “Saving does not finance Investment – Accounting as an Indispensable Guide to Economic Theory” (pdf here).

Stützel adds one additional concept, “lockstep”, which is at the core of Schmidt’s paper: if my inflow of means of payment (receipts) is equal to my cash outflow (payments) for a period, my stock of means of payment does not change; if this applies to all economic subjects, inflows and outflows of means of payment move in lockstep for the whole economy. If my net lending (increase of net financial assets) equals my net borrowing (decrease of net financial assets) for a period, my stock of net financial assets does not change (i.e. my balance on current account, mostly made up of the balance of trade, is zero). If this applies to all economic subjects, net lending and net borrowing are moving in lockstep for the whole economy. If there is lockstep both on the level of means of payment and the level of net financial assets – an empirically highly unlikely special case which can nevertheless be analytically useful – then money of any form becomes a neutral numeraire within a ‘real exchange-‘ or barter economy, as in the Walrasian tradition.

On this problem, Keynes had famously written in 1933:

“The divergence between the real-exchange economics and my desired monetary economics is, however, most marked and perhaps most important when we come to the discussion of the rate of interest and to the relation between the volume of output and the amount of expenditure.

Everyone would, of course, agree that it is in a monetary economy in my sense of the term that we actually live. Professor Pigou knows as well as anyone that wages are in fact sticky in terms of money. Marshall was perfectly aware that the existence of debts gives a high degree of practical importance to changes in the value of money. Nevertheless it is my belief that the far-reaching and in some respects fundamental differences between the conclusions of a monetary economy and those of the more simplified real-exchange economy have been greatly underestimated by the exponents of the traditional economics; with the result that the machinery of thought with which real-exchange economics has equipped the minds of practitioners in the world of affairs, and also of economists themselves, has led in practice to many erroneous conclusions and policies. The idea that it is comparatively easy to adapt the hypothetical conclusions of a real wage economics to the real world of monetary economics is a mistake. It is extraordinarily difficult to make the adaptation, and perhaps impossible without the aid of a developed theory of monetary economics.

One of the chief causes of confusion lies in the fact that the assumptions of the real-exchange economy have been tacit, and you will search treatises on real-exchange economics in vain for any express statement of the simplifications introduced or for the relationship of its hypothetical conclusions to the facts of the real world. We are not told what conditions have to be fulfilled if money is to be neutral. Nor is it easy to supply the gap.” (J.M. Keynes 1933: A Monetary Theory of Production. First published in ‘Der Stand und die nächste Zukunft der Konjunkturforschung: Festschrift für Arthur Spiethoff‘. Munich: Duncker & Humboldt, pp.123-25, full text here)

Stützel clearly identifies the implicit ‘assumption of the real exchange economy’ that renders ‘money’ ‘neutral’ in the ‘classical model’ – an assumption originally made by Walras. It is the implicit ‘lockstep’ assumption. Schmidt develops this point in detail in his paper, showing how the approaches of naive quantity theory, post-keynesian models and new keynesian models offer partial attempts to overcome the implicit lockstep assumption by modelling different partial aspects of empirical finance and the empirical financial system.

Some more information on Wolfgang Stützel’s work, one of the major foundations for the seminar and papers above, can be found in the 2019 article by Sauer & Sell: “Lost in Translation – a Revival of Wolfgang Stützel’s Mechanics of Balances” (see here). It has been among the Top 10 Most Read Articles of 2018 in the European Journal for the History of Economic Thought.

Some biographical background on Stützel: Stützel came from an entrepreneurial family. After his 1952 Ph.D. dissertation on “Price, Value and Power – Analytical Theory of the Relation between the Market and the State” and writing his foundational “Paradoxa der Geld- und Konkurrenzwirtschaft” in 1953 (which was to be published only in 1979), he worked at Berliner Bank from 1953-1956, and at Deutsche Bundesbank in 1957/58, before becoming a Professor at University of Saarland, heading the department for banking and monetary macroeconomics. He developed the foundations of his macroeconomic model during the 1950s already in his 1952 Dissertation, his 1953 “Paradoxa …” (see above) and his 1958 “Volkswirtschaftliche Saldenmechanik” (which became a classic of german macroeconomics literature), consistently refining and specifying them on through the 1980s. From 1966-1966, he was part of the german Sachverständigenrat zur Begutachtung der Gesamtwirtschaftlichen Entwicklung (German Council of Economic Experts).

So again, to read Johannes Schmidt’s paper, click here. To watch the video of Johannes Schmidt’s Oslo presentation of this paper, click here.